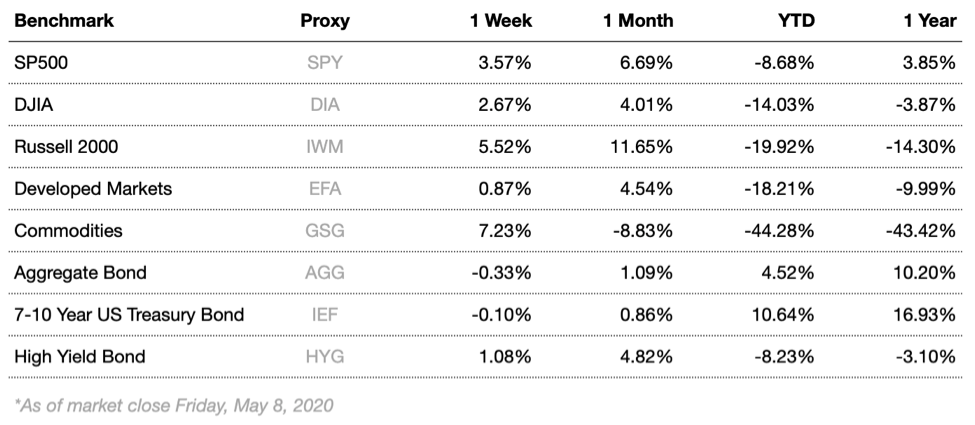

Markets rose this week and investors seem to be more encouraged at economic developments. Several U.S. states have permitted or soon will permit non-essential businesses to open in spite of the continuing Covid-19 threat. Equities finished the week up even after disastrous unemployment levels. Prices even rose Friday after unemployment reached 14.7%, a level not seen since 1940. For the second week Energy led the S&P sectors, finishing ahead of communications and materials to round out the strongest sectors. Analysts will likely continue to observe production and consumption adjustments made by market participants closely after shutdowns ground much of economic activity to a halt. Tensions with China will also remain in focus. Unemployment is likely to remain elevated for several more weeks, but economic activity is likely to begin a slow and steady return to normal in the coming weeks and months. Infection data is becoming more accurate as testing becomes more widely disseminated, helping to better assess economic options.

Overseas, markets also performed well. European countries have begun eyeing reopening their economies similarly to the U.S., likely encouraging investors. On Friday, European indices rose along with American counterparts in spite of high unemployment. All major European indices returned positive results. Japanese equities returned positive performance as well, as investors seem to be encouraged by developments surrounding the pandemic. After doing better than most developed countries initially, Japan is now starting to experience more widespread outbreaks, prompting an official state of emergency. Japan has the highest percentage of “at risk” population in the world, making containment absolutely critical.

Markets rose this week, with major equity indices bringing encouraging returns. Fears concerning global stability and health are an unexpected factor in asset values, and the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

Chart of the Week

Oil has had an impressive recovery the last two weeks. The price improvement could reflect the general optimism among investors the global economic recovery is underway, prompting support for oil prices from the demand side.

Market Update

Equities

Broad market equity indices finished the week up, with major large cap indices underperforming small cap. Economic data is still predominantly negative, but the first steps needed to see leveling out are being taken, as multiple U.S. states have reopened their economies and more are poised to do the same this month.

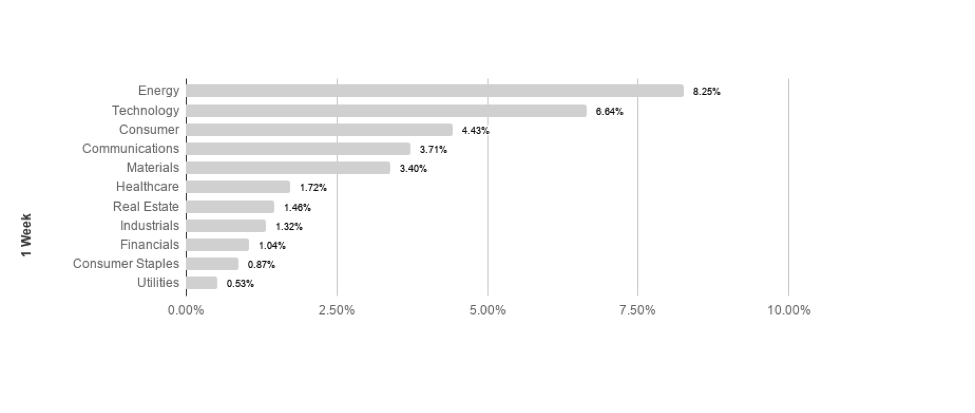

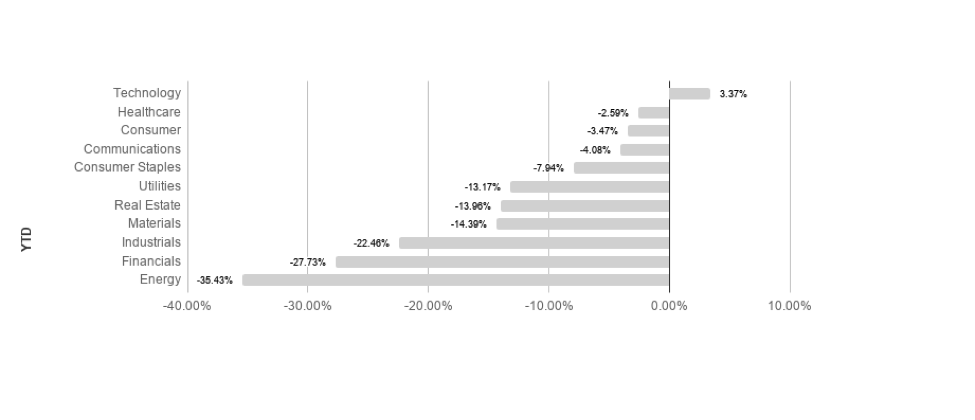

S&P sectors returned unanimously positive results this week, as broad market movements showed investor optimism amongst all sectors. For the third consecutive week, energy led the best performing sectors, followed by technology, returning 8.25% and 6.64% respectively. Consumer staples and utilities performed the worst, posting 0.87% and 0.53% respectively. Technology leads the pack so far YTD, returning 3.37% in 2020.

Commodities

Commodities rebounded further this week, driven by large gains in oil. Oil markets have been highly volatile, with investors focusing on output and consumption concerns. Global fears surrounding the virus outbreak have stoked demand concerns, as a significant impact on energy demand is expected as a result. Demand is likely to recover slowly, as countries around the globe have begun re-opening their economies. The supply side of the equation is likely to face reductions in output, as lack of storage may continue to be a problem.

Gold rose slightly this week as markets reacted to information surrounding Covid-19 and global trade. Gold is a common “safe haven” asset, typically rising during times of market stress. Focus for gold has shifted to global macroeconomics and public health concerns. Weakening real currency values resulting from massive stimulus measures may further support gold prices.

Bonds

Yields on 10-year Treasuries rose from 0.61% to 0.68% while traditional bond indices fell. Treasury yields rose as the efforts to contain the spread of Covid-19 appear to be yielding results and the economy is set to gradually reopen. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds rose slightly again this week, casing spreads to tighten. High-yield bonds are likely to remain volatile in the short to intermediate term as the Fed has adopted a remarkably accommodative monetary stance and investors flee virus risk factors, likely driving increased volatility.

Lesson to Be Learned

“The wise man bridges the gap by laying out the path by means of which he can get from where he is to where he wants to go.”

-J.P. Morgan

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

The Week Ahead

After getting a clear view at the damage to the employment market, investors will get a fresh look at the damage done to consumption. This week sees updated retail sales numbers, which will depict April’s numbers. Also on the agenda are fresh CPI number as well as weekly unemployment claims updates.

More to come soon. Stay tuned.