Markets fell slightly this week as the novel coronavirus Covid-19 continued its spread, as shutdowns and quarantines remained around the globe. After equities initially responded favorably to the passing of a $2.2 trillion federal stimulus package, investors tempered their positive outlooks in light of the rising cost of economic damages. Sectors diverged widely from each other this week as investors continue to jockey in their search for value. Energy led the S&P sectors this week, finishing ahead of consumer staples and healthcare to round out the strongest sectors. Investors are constantly adjusting to new information, creating an environment with dramatic price swings. After markets reversed a sharply negative outlook to return to an official bull market just last week, assets fell this week in response to higher than expected unemployment numbers. Public anxiety remains as the virus continues to spread. U.S. unemployment filings set an ominous new record this week beating the prior week, as now 6.6 million Americans have filed unemployment claims as a result of the economic shutdowns. Supply chains, store-front businesses, and consumer activity remain under pressure. Recent positive developments have assisted investor efforts to determine market impact as the government has recently announced the completion and delivery of new testing technology to help diagnose and isolate those infected with the disease.

Overseas, markets fell slightly more than U.S. indices, as European markets fell in light of increasing infection rates. Italy has been hit especially hard by the virus, as they have the oldest average population in Europe. Developments in Italy have been encouraging, as deaths and new infections appear to be in decline. All major European indices returned negative results. Japanese equities also returned sharply negative performance, outpacing all other developed economies with the worst weekly returns. After doing better than most developed countries initially, Japan is now starting to experience widespread outbreaks, prompting a likely state of emergency. Japan has the highest percentage of “at risk” population in the world, making containment absolutely critical.

Markets fell this week, with all major equity indices bringing in negative returns. Fears concerning global stability and health are an unexpected factor in asset values, and the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

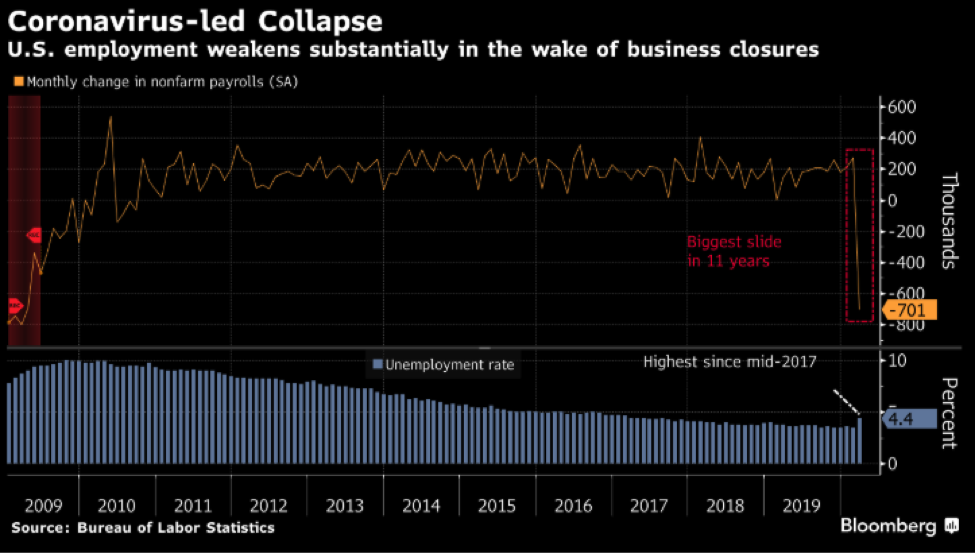

Chart of the Week

Since the outbreak of the Covid-19 coronavirus, the labor market has declined dramatically. Shut-downs and quarantines have begun taking their toll, as millions of Americans have filed for unemployment, causing the unemployment rate to spike to 4.4%.

Market Update

Equities

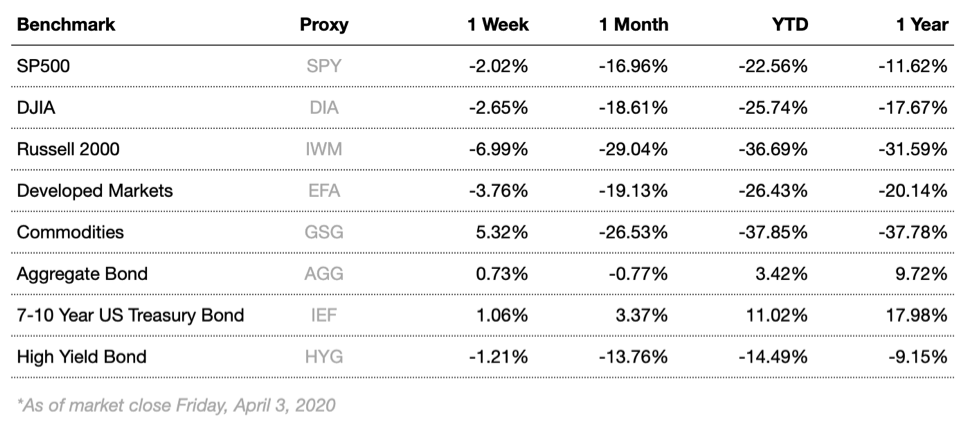

Broad market equity indices finished the week down, with major large cap indices outperforming small cap. Recent fears returned this week, as prices fell in response to rising unemployment claims. Other economic data has come in above expectations, as both consumer confidence and manufacturing PMI (purchasing managers index) surprised analysts, possibly providing encouragement surrounding the market as a whole.

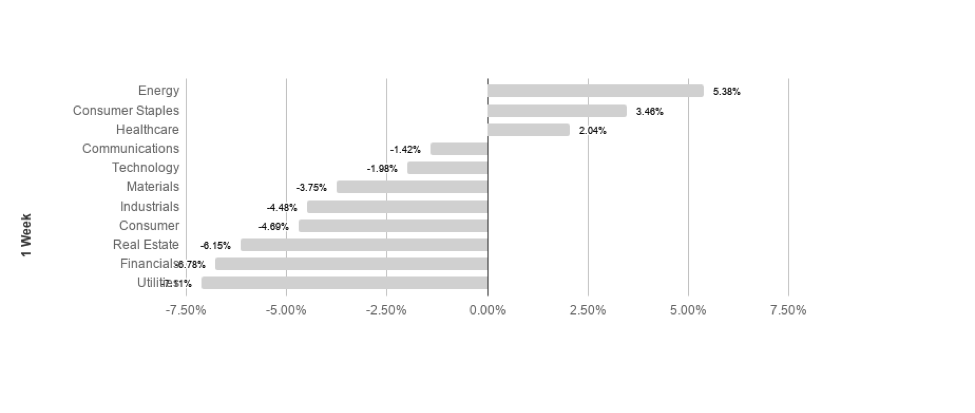

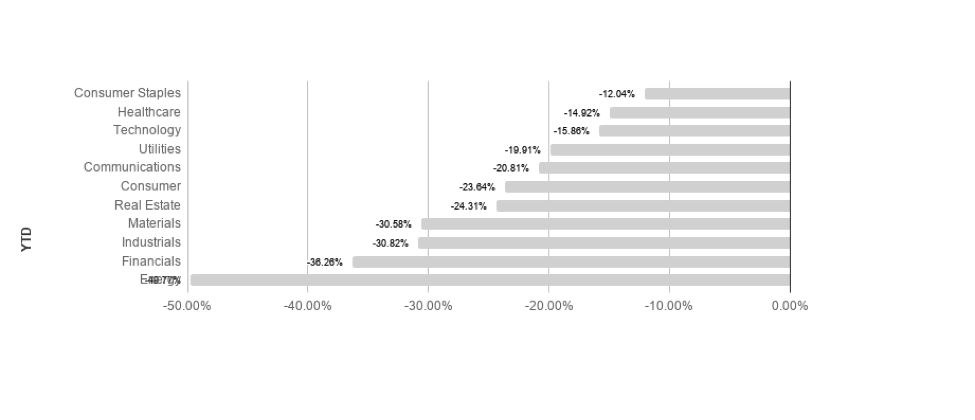

S&P sectors returned mixed results this week, as broad market movements showed investors shifting between sectors. Energy and consumer staples led the best performing sectors returning 5.38% and 3.46% respectively. Financials and utilities performed the worst, posting -6.78% and -7.11% respectively. Consumer staples now leads the pack so far YTD, returning -12.04% in 2020.

Commodities

Commodities climbed this week, propelled by gains in oil. Oil markets have been highly volatile, with investors focusing on geopolitical tension and global demand concerns. Global fears surrounding the virus outbreak have stoked demand concerns, as a significant impact on energy demand is expected as a result. Oil prices may get some much needed support from the supply side, as it is expected that Russian and Saudi Arabia will end their price war.

Gold declined negligibly this week as fear surrounding the coronavirus increased. Gold is a common “safe haven” asset, typically rising during times of market stress. Focus for gold has shifted to global macroeconomics and public health concerns.

Bonds

Yields on 10-year Treasuries fell considerably to 0.59% from 0.67% while traditional bond indices rose. Treasury yields fell as virus fears spread and investors try to protect against increasing risk. An additional layer of influence on treasury yields is the newly passed federal stimulus bill. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds dropped again this week, causing spreads to loosen. High-yield bonds are likely to remain volatile in the short to intermediate term as the Fed has adopted a remarkably accommodative monetary stance and investors flee virus risk factors, likely driving increased volatility.

Lesson to Be Learned

“Beware the investment activity that produces applause; the great moves are usually greeted by yawns.”

-Warren Buffet

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

The Week Ahead

Markets continue to face the same uncertainty surrounding the coronavirus. While the infection seems to have peaked in some places, it’s still on the rise in others. This week’s economic calendar includes updated CPI, University of Michigan consumer confidence numbers, and new unemployment claims.

More to come soon. Stay tuned.