Stocks rose this week even as nonfarm payrolls came in well under expectations in November. Markets continue to be encouraged by the progress in COVID-19 vaccine situation, and many countries will begin administering vaccines this month. Globally, COVID-19 infections continue to increase, underscoring the positive impact successful vaccinations will likely have on the global economy. New daily infections in the U.S. remain stubbornly above 100K, and new infections in December have now crossed the 200K mark for the first time. Economic data was mixed this week with unemployment claims and the unemployment rate beating expectations, but with November hiring disappointing analysts. Unemployment claims have been choppy but moving downwards, likely indicating slowly recovering labor markets. Recently, unemployment declines have slowed somewhat, prompting questions as to whether or not the recovery may be coming to a halt. The persistently high and increasing case rates of COVID-19 in the U.S. remain concerning, and restrictive measures have been reinstated in some areas. With vaccines being administered in the near future, hopefully economic activity can resume normally sooner than later.

Overseas, developed markets and emerging markets both rose. Japan and most of Europe responded favorably to macroeconomic developments, and with vaccinations beginning, there will likely be increasing hopes that lockdowns in Europe will end sooner than later.

Markets performed well this week, with equity indices bringing in positive returns. Fears concerning global stability and health are an unexpected factor in asset values, and the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

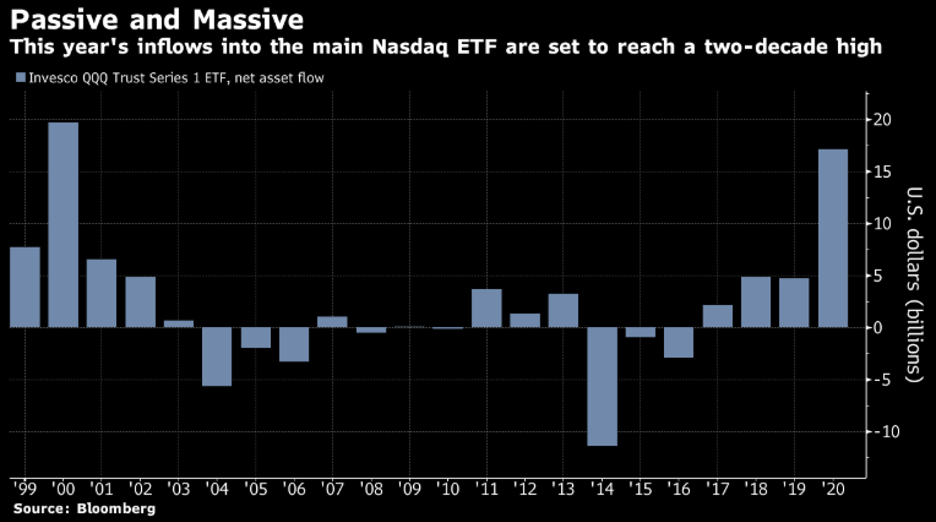

Chart of the Week

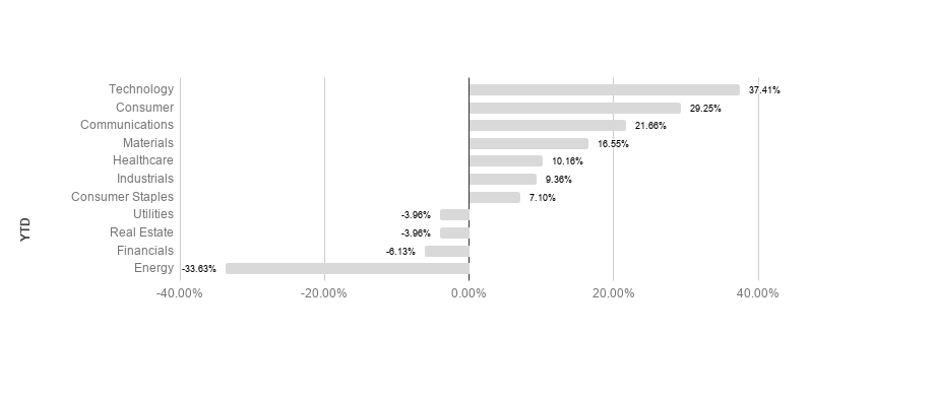

The Nasdaq composite index has skyrocketed this year, drawing the largest capital inflows into the Nasdaq tracking QQQ ETF since the dotcom bubble. Tech stocks have propelled the rise, as the technology sector is up 37.41% YTD.

Market Update

Equities

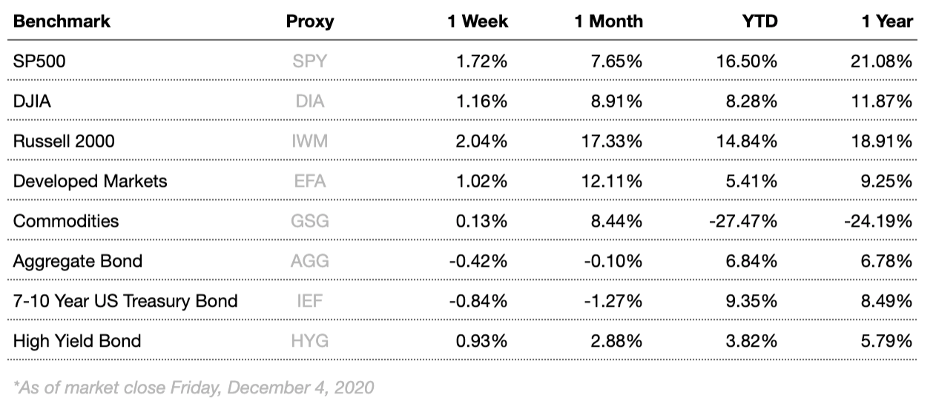

Broad market equity indices finished the week positive, with major large cap indices slightly underperforming small cap. Economic data has been solid, but the global recovery has a long way to go to recover from COVID-19 lockdowns.

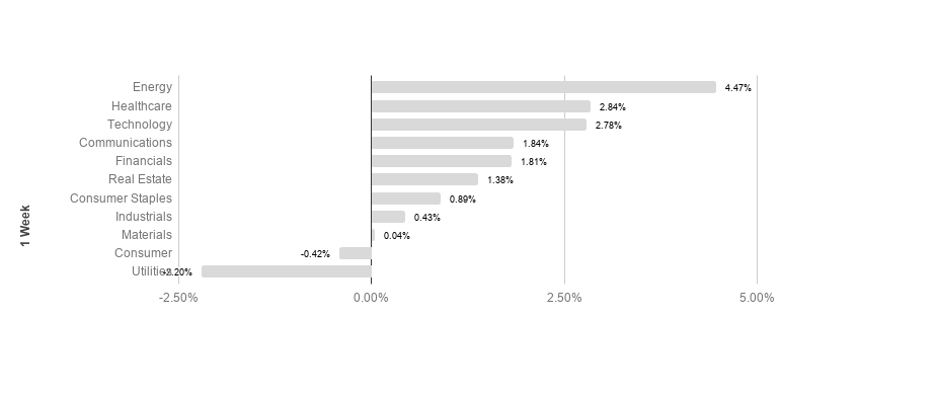

S&P sectors returned mostly positive results this week. Energy and healthcare outperformed, returning 4.47% and 2.84% respectively. Consumer discretionary and utilities underperformed, posting -0.42% and -2.20% respectively. Technology leads the pack so far YTD, returning 37.41% in 2020.

Commodities

Commodities rose this week, driven by a rise in oil prices. Oil markets have begun to show a significant responsiveness to the status of vaccine development efforts, as normal economic conditions are critical to energy consumption. Now that vaccines are now being administered, oil prices have reached levels not seen since pre-pandemic. Energy markets have been highly volatile, but it appears that some stability may be on the horizon given recent developments. Demand is still likely to remain under pressure however, as lockdown restrictions in Europe as well as the U.S. have squeezed consumption. On the supply side, operating oil rigs are still well under early 2020 numbers, but trending upwards.

Gold rose this week as the U.S. dollar weakened. Gold is a common “safe haven” asset, typically rising during times of market stress. Focus for gold has shifted to global macroeconomics surrounding COVID-19 damage and recovery efforts. Recent declines in the precious metal could indicate increasing risk appetites.

Bonds

Yields on 10-year Treasuries rose this week from 0.84% to 0.97% while traditional bond indices fell. Treasury yield movements reflect general risk outlook, and tend to track overall investor sentiment. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds rose this week as spreads tightened. High-yield bonds are likely to remain volatile in the short to intermediate term as the Fed has adopted a remarkably accommodative monetary stance and investors warm slightly to economic risk factors, likely driving increased volatility.

Lesson to Be Learned

“The individual investor should act consistently as an investor and not as a speculator. This means … that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money’s worth for his purchase.”

-Ben Graham

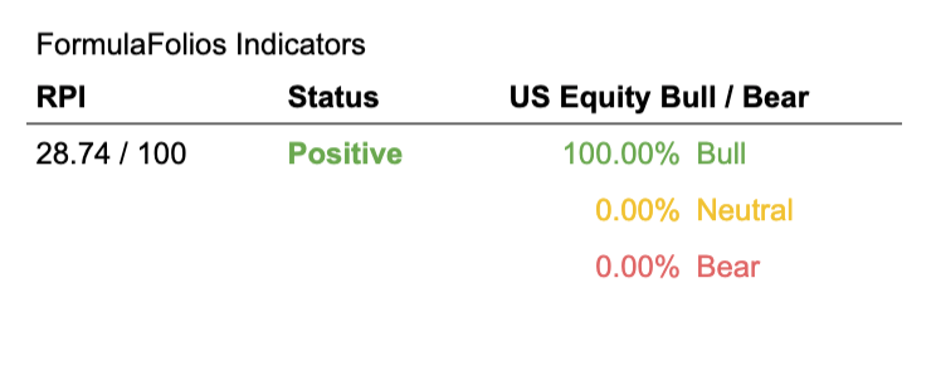

We have two simple indicators we share that help you see how the economy is doing (we call this the Recession Probability Index, or RPI), as well as if the US Stock Market is strong (bull) or weak (bear).

In a nutshell, we want the RPI to be low on a scale of 1 to 100. For the US Equity Bull/Bear indicator, we want it to read at least 66.67% bullish. When those two things occur, our research shows market performance is typically stronger, with less volatility.

The Recession Probability Index (RPI) has a current reading of 28.74, forecasting a lower potential for an economic contraction (warning of recession risk). The Bull/Bear indicator is currently 100% bullish, meaning the indicator shows there is a slightly higher than average likelihood of stock market increases in the near term (within the next 18 months).

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

The Week Ahead

This week is light on high impact economic releases. Analysts may still be encouraged by upbeat CPI and PPI numbers, and further declining unemployment claims would also be a welcome development.

More to come soon. Stay tuned.