Markets fell dramatically this week as investors grapple with the Coronavirus. Communications led the S&P sectors this week with the smallest losses, finishing ahead of consumer staples and healthcare to round out the strongest sectors. Markets have turned fearful concerning developments regarding the spread of the Coronavirus, as new cases have begun emerging around the globe. Public anxiety remains as the virus continues to spread, adding pressure to markets and global supply chains as both consumers and workers are staying home.

European indices declined this week, with all major indices returning negative results. Japanese equities also returned negative performance, continuing last week’s trend. New cases of Coronavirus have been identified in both Europe and Asia, causing elevated volatility and increased selling pressure on assets.

Markets retreated this week, with all major equity indices bringing in negative returns. Fears concerning global stability and health are an unexpected factor in asset values, and the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

Chart of the Week

Chinese manufacturing has been crushed under the weight of the recent Coronavirus outbreak. Such an extreme plunge will likely fuel concerns that damage to the world’s second largest economy may be severe and not short lived.

Market Update

Equities

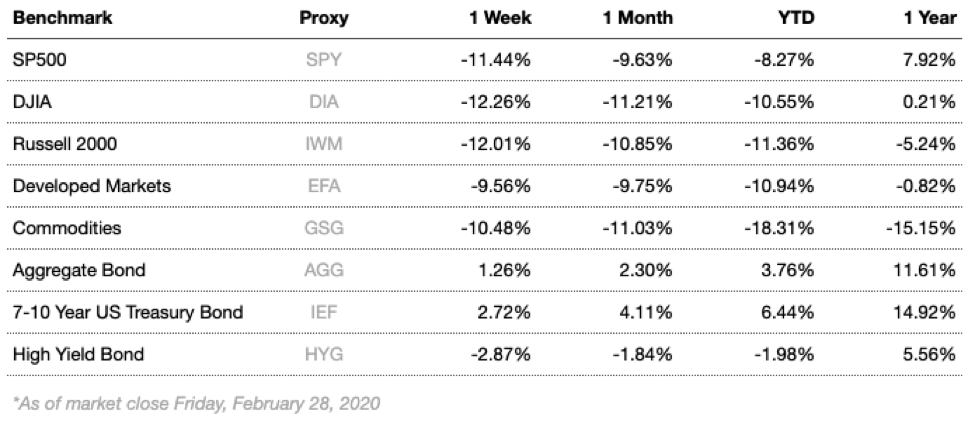

Broad market equity indices finished the week negative, with major large cap indices performing similarly to small cap. Recent fears weighed on equities this week, as prices declined in response to global economic concerns resulting from the further spread of the coronavirus.

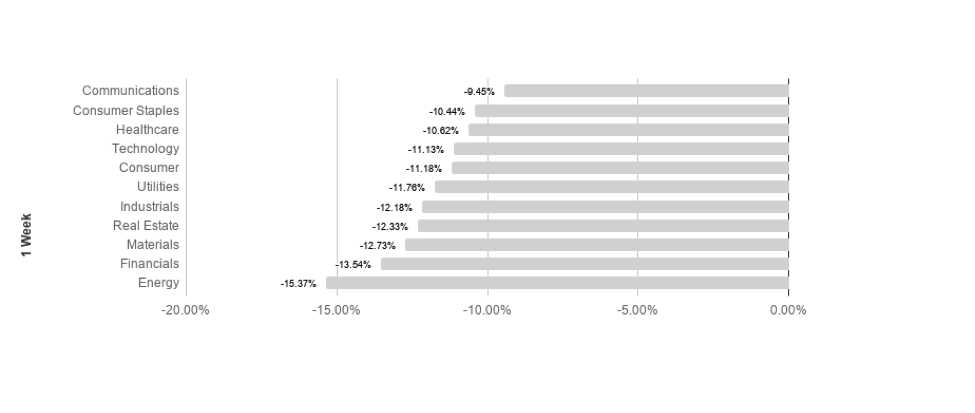

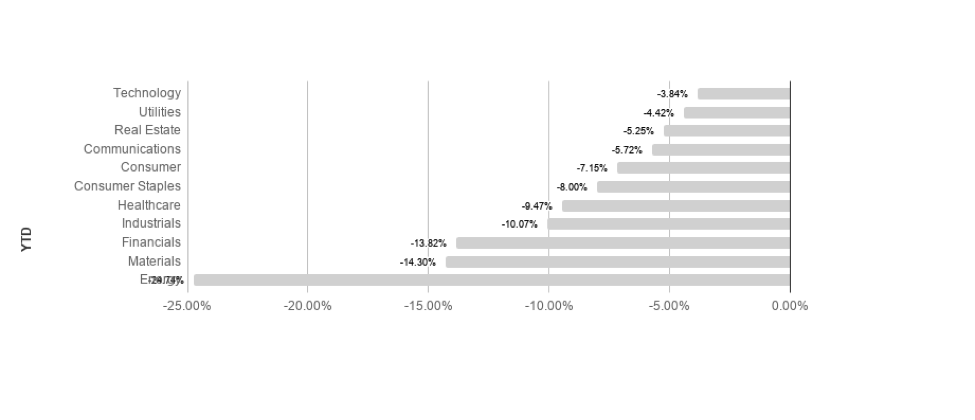

No S&P sectors returned positive results this week, as the broad market sell off spared no sector. Communications and consumer staples led the best performing sectors returning -9.45% and -10.44% respectively. Energy and financials underperformed the most, losing -15.37% and -13.54% respectively. Technology has lost the least ground so far YTD, returning -3.84% in 2020.

Commodities

Commodities dropped this week, driven by losses in gold, oil, and natural gas. Oil markets have been highly volatile, with investors focusing on geopolitical tension and global demand concerns. Global fears surrounding the virus outbreak have further stoked demand concerns, as a significant impact on energy demand is expected as a result. Weakened demand in an already challenging global market has driven oil to the lowest prices seen since 2018.

Gold fell this week as fear surrounding the Coronavirus increased. The decline in gold prices is unusual, as it seemingly defies its status as a “safe haven” asset. Focus for gold has shifted to global growth and public health concerns, as geopolitical tensions seem to be fading from investor focus.

Bonds

Yields on 10-year Treasuries dropped considerably to 1.15% from 1.47% while traditional bond indices rose. Treasury yields fell as investors try to protect against the prospect of a global virus outbreak. The 10-2 year yield spreads widened. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds dropped this week, causing spreads to widen. High-yield bonds are likely to remain volatile in the short to intermediate term as the Fed has not adjusted its neutral monetary stance and investors flee virus risk factors, likely driving increased volatility.

Lesson to Be Learned

“Spend each day trying to be a little wiser than you were when you woke up.”

-Charlie Munger

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

FormulaFolios Indicators

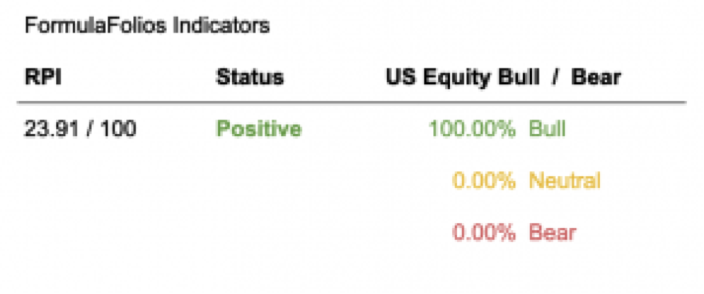

We have two simple indicators we share that help you see how the economy is doing (we call this the Recession Probability Index, or RPI), as well as if the US Stock Market is strong (bull) or weak (bear).

In a nutshell, we want the RPI to be low on the scale of 1 to 100. For the US Equity Bull/Bear indicator, we want it to read least 66.67% bullish. When those two things occur, our research shows market performance is strongest and least volatile.

The Recession Probability Index (RPI) has a current reading of 23.91, forecasting further economic growth and not warning of a recession at this time. The Bull/Bear indicator is currently 100% bullish – 0% bearish, meaning the indicator shows there is a slightly higher than average likelihood of stock market increases in the near term (within the next 18 months).

The Week Ahead

The economic calendar sees updated employment and non-manufacturing PMI this week, but prices will likely be dominated by developments surrounding the Coronavirus. Three FOMC members will also be speaking at events this week, possibly revealing Fed perspectives on the impact of the virus outbreak and whether monetary policy will need adjusting.

More to come soon. Stay tuned.