Markets paused somewhat this week as investors responded to the evolving Coronavirus situation. Utilities led the S&P sectors this week with considerable gains, finishing ahead of consumer staples and healthcare to round out the strongest sectors. Markets have turned fearful concerning developments regarding the spread of the Coronavirus, as new cases have begun emerging around the globe. Public anxiety remains as the virus continues to spread, adding pressure to markets and global supply chains as both consumers and workers are staying home. Investors have faced challenges to determining market impact, as there is still very little known about the novel virus.

European indices declined this week, with all major indices returning negative results. Japanese equities also returned negative performance, continuing last week’s trend. New cases of Coronavirus have been identified in both Europe and Asia, causing elevated volatility and increased selling pressure on assets.

Markets mostly retreated this week, with many major equity indices bringing in negative returns. Fears concerning global stability and health are an unexpected factor in asset values, and the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

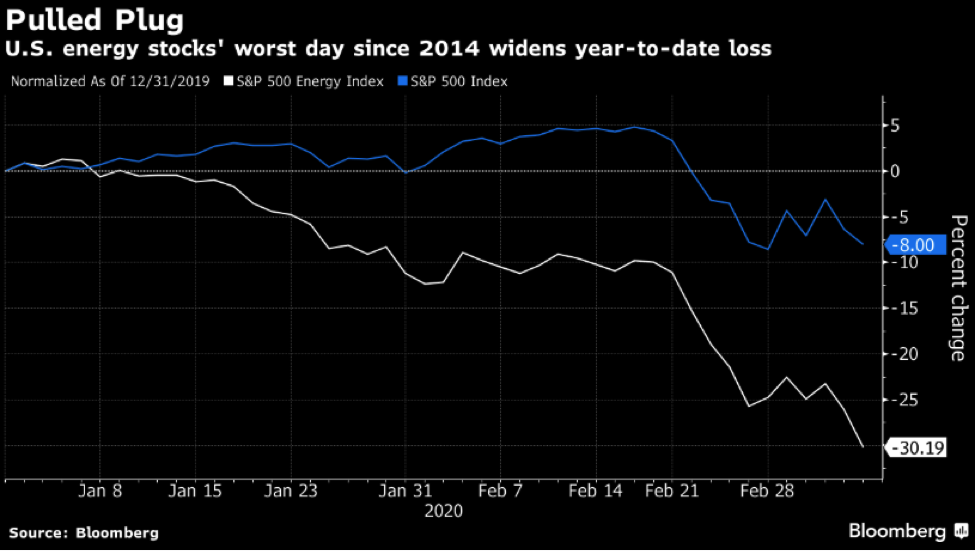

Chart of the Week

Energy stocks have been hit especially hard by the market downturn. Already under pressure from perennially low commodity prices, the recent drop has pushed the sector into new lows, adding new strain to the already struggling industry.

Market Update

Equities

Broad market equity indices finished the week mixed, with major large cap indices outperforming small cap. While recent fears continued to weigh on equities this week, prices were mixed in response to Coronavirus developments. A positive U.S. jobs report helped buoy U.S. markets in spite of global economic health concerns.

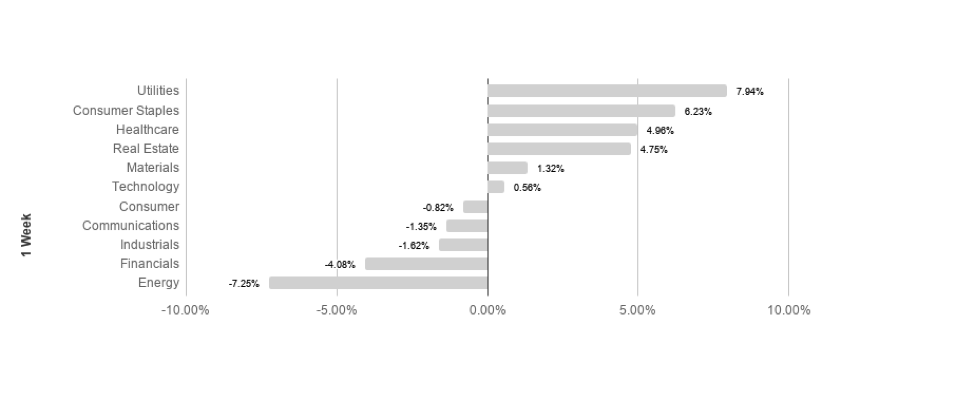

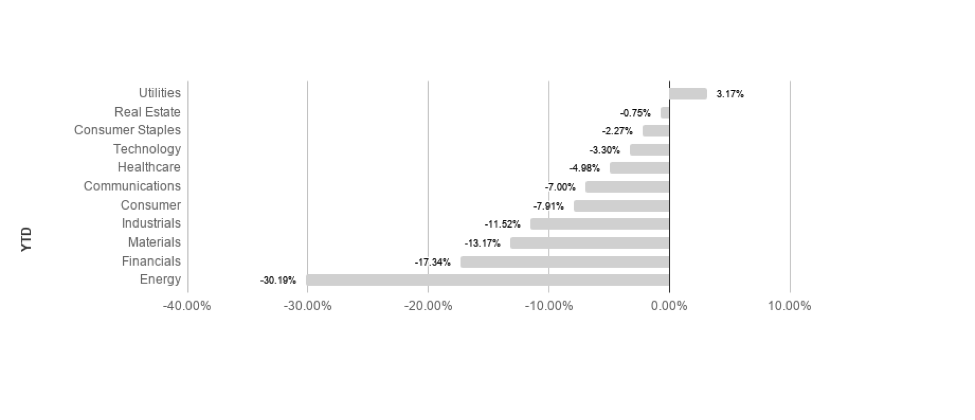

S&P sectors returned mixed results this week, as broad market movements varied. Utilities and consumer staples led the best performing sectors returning 7.94% and 6.23% respectively. Energy and financials underperformed the most, losing -7.25% and -4.08% respectively. Utilities lead the pack so far YTD, returning 3.17% in 2020.

Commodities

Commodities dropped this week, driven by dramatic losses in oil. Oil markets have been highly volatile, with investors focusing on geopolitical tension and global demand concerns. Global fears surrounding the virus outbreak have further stoked demand concerns, as a significant impact on energy demand is expected as a result. This compelled OPEC to hold an emergency meeting this week, with Saudi Arabia pushing for an output cut to buoy oil prices. Russia refused to agree to cuts, sending prices to new lows.

Gold rose this week as fear surrounding the Coronavirus increased. Gold is a common “safe haven” asset, typically rising during times of market stress. Focus for gold has shifted to global growth and public health concerns, as geopolitical tensions seem to be fading from investor focus.

Bonds

Yields on 10-year Treasuries dropped considerably to .76% from 1.15% while traditional bond indices rose. Treasury yields fell as investors try to protect against the prospect of a global virus outbreak. The 10-2 year yield spreads widened. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds dropped slightly this week, causing spreads to widen. High-yield bonds are likely to remain volatile in the short to intermediate term as the Fed has not adjusted its neutral monetary stance and investors flee virus risk factors, likely driving increased volatility.

Lesson to Be Learned

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.”

-Robert Kiyosaki

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission-critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

The Week Ahead

The economic calendar is light this week, with CPI and retail sales being the only high impact releases scheduled. We expect continued volatility as markets continue to process developments surrounding the Coronavirus.

More to come soon. Stay tuned.