Markets were mixed this week as Q2 GDP numbers disappointed analysts. Expectations were for growth to come in around 8.5% annualized, but growth registered just 6.5%. To be clear, 6.5% is incredible quarterly growth, but an expectations miss in growth projections of more than 20% is unusual. The Fed meeting and press conference appeared to begin laying the groundwork for tapering its asset purchase program, but current bond purchases will remain as-is for the near future. The PCE deflator came in below expectations, hopefully cooling concerns over inflation. COVID-19 cases have been rising nationally again, with most new cases being attributed to the “Delta” variant, but so far deaths have not been spiking, a new development that likely can be attributed to large swaths of the population having been vaccinated. Overall, the economy is well positioned to continue recovering from pandemic lockdowns, but inflation risks as well as labor challenges and production capacity are eating into productivity.

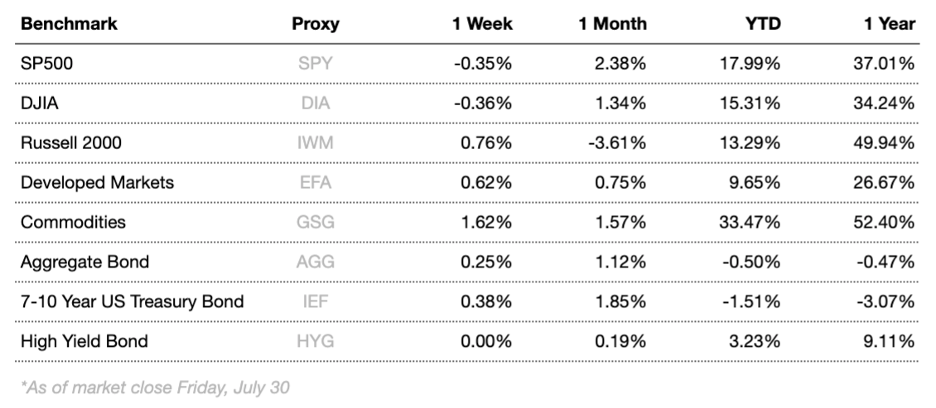

Overseas, developed markets outperformed emerging markets, with developed indices returning positive performance and emerging markets returning negative performance. European indices were mixed, while Japanese markets returned negative performance for the week. Improving prospects against the pandemic as well as improved prospects for economic recovery should continue to help lift markets globally over time.

Markets were mixed this week as investors continue to assess the state of the global economy. While fears concerning global stability and health appear to be in decline, the recent volatility serves as a great reminder of why it is so important to remain committed to a long-term plan and maintain a well-diversified portfolio. When stocks were struggling to gain traction last month, other asset classes such as gold, REITs, and US Treasury bonds proved to be more stable. flashy news headlines can make it tempting to make knee-jerk decisions, but sticking to a strategy and maintaining a portfolio consistent with your goals and risk tolerance can lead to smoother returns and a better probability for long-term success.

Chart of the Week

European stocks have been on a hot streak, registering six months of price gains. Investors have been upbeat about the recovery and growth prospects in Europe.

Market Update

Equities

Broad market equity indices finished the week mixed, with major large cap indices underperforming small cap. Economic data has been mostly encouraging, but the global recovery has a long way to go to recover from COVID-19 lockdowns.

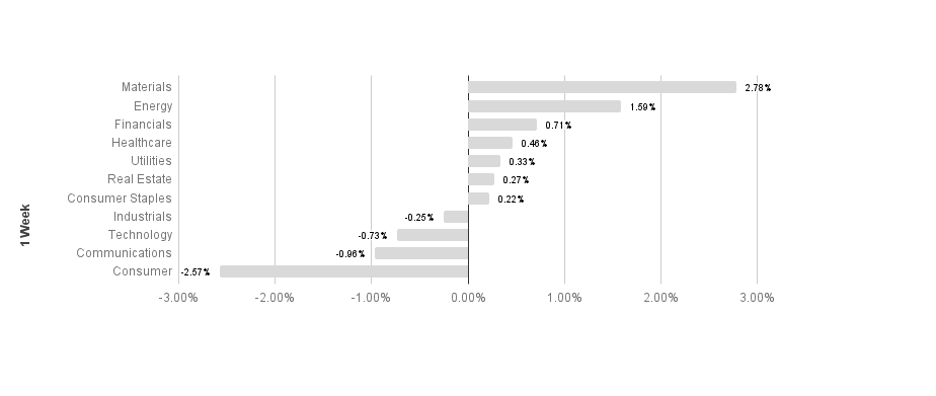

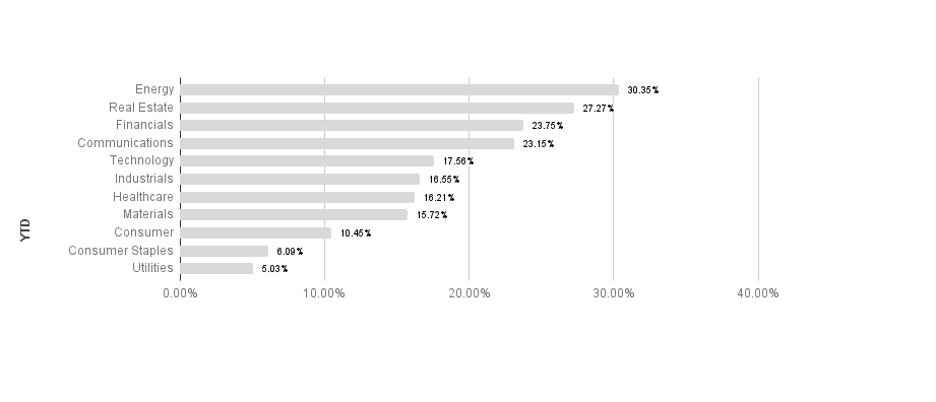

S&P sectors were mixed this week. Materials and energy outperformed, returning 2.78% and 1.59% respectively. Energy and utilities underperformed, posting -0.96% and -2.57% respectively. Energy maintains its lead in 2021 with a 30.35% return.

Commodities

Oil rose this week as crude oil inventories shrunk more than expected. Energy markets have been highly volatile in the COVID era, but it appears that higher oil prices may be more of the norm given recent market fundamentals. Demand is still low compared to early 2020, but as global economies are continuing to open up, oil consumption is recovering rapidly. On the supply side, operating oil rigs are still well under early 2020 numbers, but trending upwards. In addition to supply and demand, a volatile dollar is likely to have a large impact on commodity prices. OPEC has recently agreed to a new deal to increase output, which should help put downward pressure on oil prices.

Gold rose slightly this week as the U.S. dollar weakened. Gold is a common “safe haven” asset, typically rising during times of market stress. Focus for gold has shifted again to include not just global macroeconomics surrounding COVID-19 damage and recovery efforts, but also inflation and its possible impact on U.S. dollar value.

Bonds

Yields on 10-year Treasuries fell this week from 1.2763 to 1.2223 while traditional bond indices rose. Treasury yield movements reflect general risk outlook, and tend to track overall investor sentiment. Expected increases in future inflation risk have helped elevate yields since pandemic era lows in rates. Treasury yields will continue to be a focus as analysts watch for signs of changing market conditions.

High-yield bonds remained unchanged this week as spreads loosened. High-yield bonds are likely to remain more stable in the short to intermediate term as the Fed has adopted a remarkably accommodative monetary stance and major economic risk factors subside, likely helping stabilize volatility.

Lesson to Be Learned

“The individual investor should act consistently as an investor and not as a speculator. This means … that he should be able to justify every purchase he makes and each price he pays by impersonal, objective reasoning that satisfies him that he is getting more than his money’s worth for his purchase.”

-Ben Graham

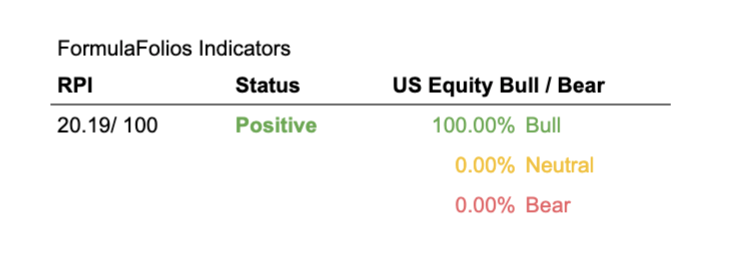

FormulaFolios has two simple indicators we share that help you see how the economy is doing (we call this the Recession Probability Index, or RPI), as well as if the US Stock Market is strong (bull) or weak (bear).

In a nutshell, we want the RPI to be low on a scale of 1 to 100. For the US Equity Bull/Bear indicator, we want it to read at least 66.67% bullish. When those two things occur, our research shows market performance is typically stronger, with less volatility.

The Recession Probability Index (RPI) has a current reading of 20.19, forecasting a lower potential for an economic contraction (warning of recession risk). The Bull/Bear indicator is currently 100% bullish, meaning the indicator shows there is a slightly higher than average likelihood of stock market increases in the near term (within the next 18 months).

It can be easy to become distracted from our long-term goals and chase returns when markets are volatile and uncertain. It is because of the allure of these distractions that having a plan and remaining disciplined is mission critical for long term success. Focusing on the long-run can help minimize the negative impact emotions can have on your portfolio and increase your chances for success over time.

The Week Ahead

This week sees updated PMI numbers as well as nonfarm payroll figures and official unemployment rates.

More to come soon. Stay tuned.